What return can you get renting a 4-bedroom house in Rio Vermelho Florianópolis to a family?

Four-bedroom houses in Rio Vermelho, Florianópolis typically rent for R$3,500–5,500 monthly to families and remote professionals, yielding 6–8% net return after management fees (8–10% of rent) and property tax. Actual yields depend on property condition, location within the neighbourhood, and local market conditions. This segment attracts longer-term tenants (12+ months) compared to beachfront apartments, reducing vacancy risk but not eliminating it. Professional management is essential for foreign owners managing from outside Brazil.

The Shift Away from Beachfront Speculation

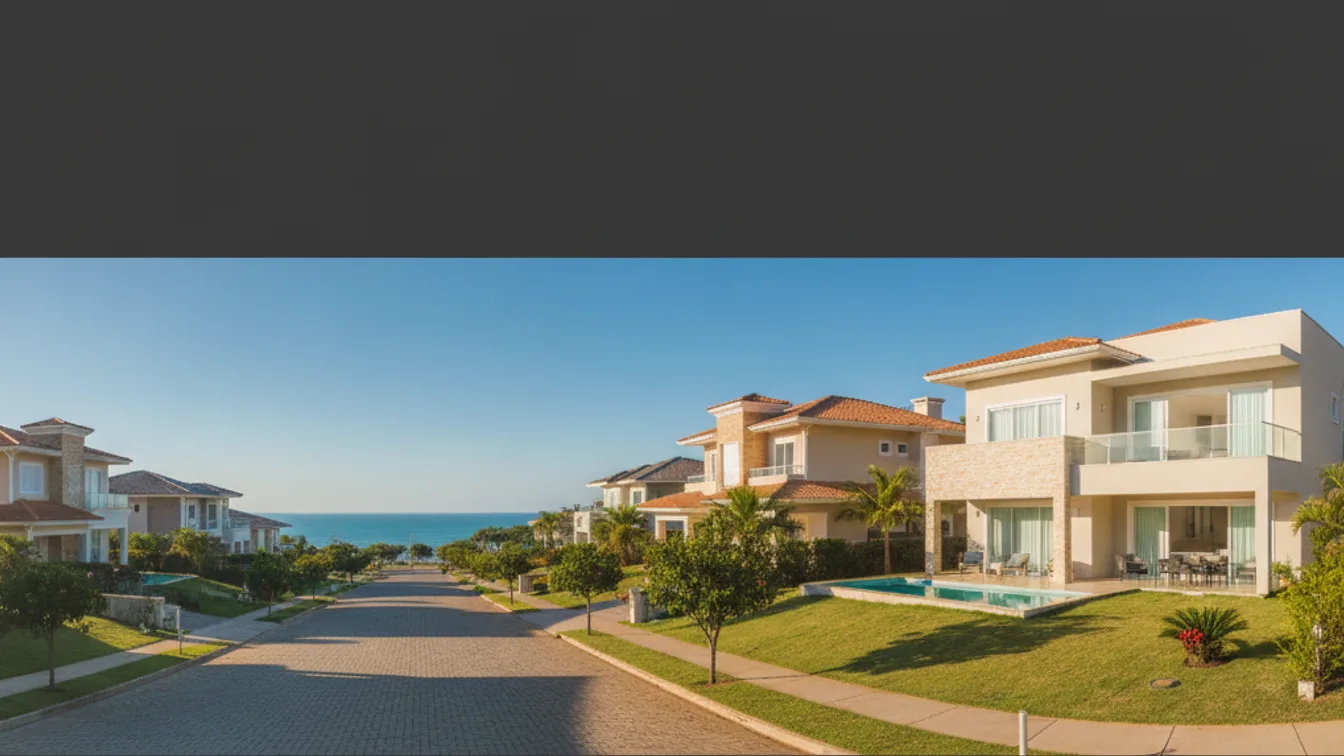

When I first arrived in Florianópolis from Punta del Este, I expected to see capital flowing toward the obvious: beachfront towers, penthouses, the coastal prestige play. Instead, I've watched a quieter movement emerge. Uruguayan and Argentine investors—the same clients I served in private banking—are increasingly drawn to four-plus-bedroom houses in Rio Vermelho, a residential neighbourhood that sits deliberately inland from the tourist machinery. This is not accidental. It reflects something more durable than seasonal speculation: a recognition that family-oriented residential property, priced below the coastal supercycle, offers better fundamentals and lower currency risk over a decade.

Rio Vermelho occupies a peculiar position in Florianópolis's geography. It is neither beachfront nor remote. It is residential, walkable, and suburban in the gentlest sense—close enough to dining and services, far enough from the transience of tourism. Properties here, particularly substantial four-bedroom houses, attract a different tenant profile than beach apartments: families, remote professionals, executives relocating for contract work. These are renters who stay 12+ months, who respect a property, who treat it as a home rather than a hotel room.

Why Family Homes Matter More Than You Think

From a wealth preservation standpoint—which is always my lens—this matters enormously. As of July 2026, Rocks's integrated catalog shows Florianópolis's median property price stands at R$1.65 million, with average pricing per square metre at R$14,818. That figure includes everything: penthouses in Lagoa da Conceição, modest one-bedrooms in older areas, and yes, the substantial family houses of Rio Vermelho. The segment we're discussing sits comfortably in the R$500,000–R$900,000 range, which places it in a fundamentally different risk class than either budget stock or luxury waterfront. You are not speculating on a development cycle. You are not betting on international tourism recovery or pandemic patterns. You are holding a tangible asset with recurring tenant demand.

Why does this appeal to Uruguayan investors specifically? Because we understand the importance of income stability. In Punta del Este, a similar four-bedroom house in a family neighbourhood might command R$1.2–1.5 million today, with lower rental yield and seasonal volatility. Here, you can acquire equivalent quality for 30–40% less capital, with year-round residential demand and professional management infrastructure that has matured significantly since 2019.

The Professional Management Question

I must be precise here: holding rental property in Brazil from Montevideo requires non-negotiable professional management. This is not optional. A competent property manager in Florianópolis will charge 8–10% of monthly rent, coordinate with the Receita Federal, and ensure compliance with both Brazilian tax requirements and your Uruguayan reporting obligations. A four-bedroom house in Rio Vermelho, well-positioned, typically rents for R$3,500–5,500 monthly, depending on finish and proximity to key neighbourhoods. After management fees and property tax, net yield historically falls in the 6–8% range. That is not venture capital. It is wealth preservation with income attached.

One concrete example illustrates the segment: the Brutalist-Style Smart Home with Private Garden currently listed in Rio Vermelho combines solid architecture, contemporary automation, and a footprint that appeals to families seeking both space and modern amenities. This is the profile driving quiet demand—not architectural fame, but durability and function.

The Broader Diversification Logic

El largo plazo siempre gana. The long game always wins. When I speak with investors who have capital deployed across both Uruguay and Brazil, the pattern is consistent: keep 60–70% in Uruguayan property or fixed-rate Uruguayan instruments for capital preservation, deploy 30–40% into Brazilian coastal residential for appreciation and rental income. Rio Vermelho's four-bedroom houses fit that second allocation cleanly. They are not the flashy growth play; they are the reliable income generator and hedge against BRL volatility.

The fact that foreign investors hold equal property rights in Brazil is often overlooked. You are not a secondary buyer. You have the same legal standing as a Brazilian national. Add an 11-year tax holiday available to qualifying Brazilian real estate investors (yes, this includes foreigners meeting the criteria), and the after-tax arithmetic improves considerably.

A Quiet Market Speaking Volumes

The rising interest we're observing in Rio Vermelho's residential segment reflects mature investor thinking. These are buyers who have stopped chasing headlines and started chasing fundamentals: long-term tenant demand, diversification across two stable LatAm economies, currency hedging, and income generation in a neighbourhood that does not depend on seasonal tourism to function.

Diversificar no es un lujo—es prudencia. Diversification is not luxury; it is prudence. When you're ready to explore this segment in depth, I'm here to walk through the numbers, the tax structure, and the management framework that makes it work.

Cuando estén listos, estoy aquí para conversar.