A 30% Down Payment, a 10-Year Plan, and No Local Credit History Required

In Miami, securing an oceanfront unit typically means a 40% down payment and a grueling underwriting process that can stretch for months. In Santa Catarina, buyers are locking in high-growth coastal properties with 30% down and payment plans stretching up to 10 years — often with minimal paperwork. I've seen this pattern before — in Manhattan, in Miami, and now here. This kind of financing flexibility is one of the core reasons I remain firmly convinced that SC is the best risk-adjusted international real estate opportunity currently available.

For international buyers, financing real estate in Brazil can look intimidating at first glance. Currency differences, local banking regulations, and conservative lending practices all create the impression that credit access is limited. The reality is quite different — particularly when you know which route to take.

1. Developer Financing: The Most Practical Route for International Buyers

For the vast majority of my international clients, developer financing is the fastest, simplest, and least bureaucratic path to ownership in Brazil. At Rocks Investments, this is frequently our preferred structure — especially for buyers who prioritize speed, flexibility, and minimal friction.

Why developer financing stands out:

- Minimal documentation required

- No Brazilian credit history needed

- Fully accessible to non-residents

- Flexible, negotiable payment structures

- Widely available across high-growth coastal markets in Santa Catarina

Unlike traditional banks, developers are motivated to move units. That motivation translates directly into favorable, negotiable payment terms for buyers.

How Developer Payment Plans Work

Developer financing is most commonly associated with off-plan (pre-construction) properties, but it extends beyond that.

During Construction (Off-Plan)

- Payments are distributed across the construction timeline

- Lower upfront capital outlay required

- Strong appreciation potential before delivery

Extended Payment Plans (Post-Delivery)

- Some developers allow payments to continue after the unit is completed

- Buyers can generate rental income while still servicing the balance

- Particularly attractive from a portfolio cash flow perspective

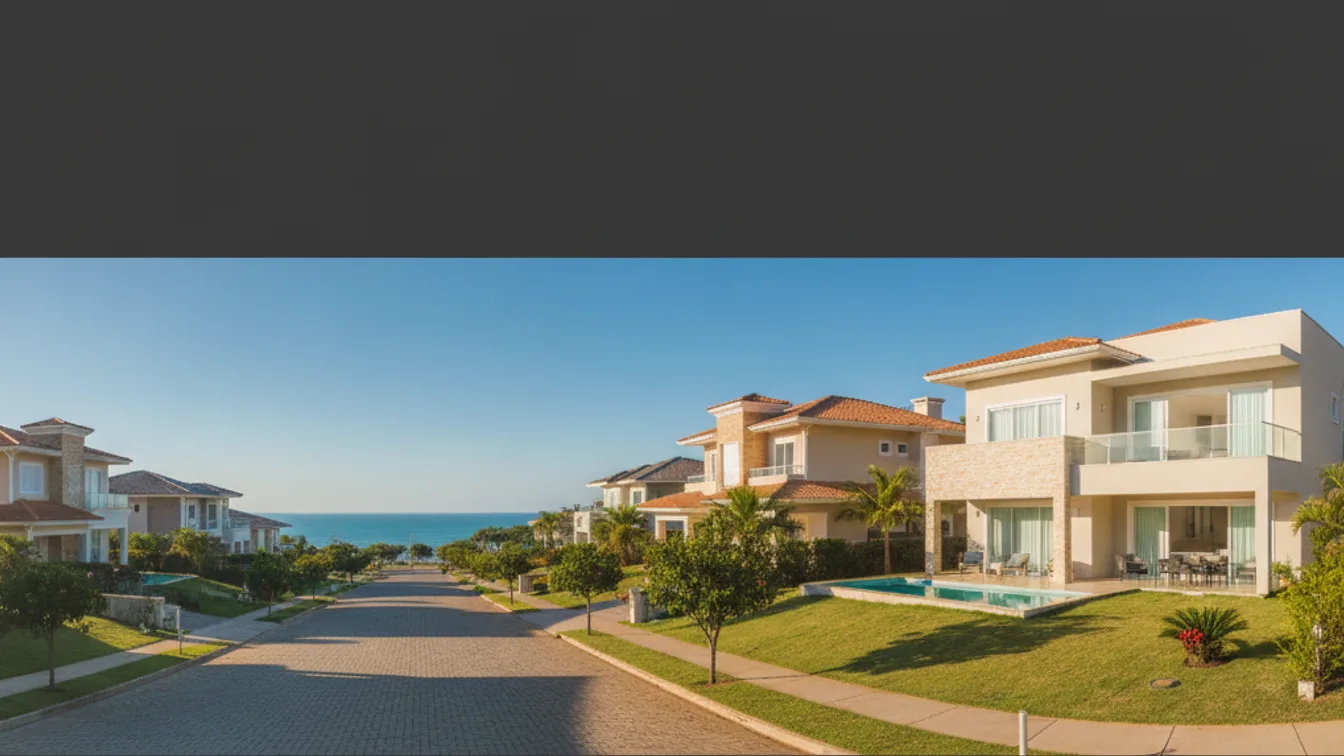

Real Examples in Santa Catarina

Itajaí (Praia Brava region)

- Units delivering in approximately 2 months

- 30% down payment

- Up to 120-month (10-year) payment plan

Biguaçu (near Florianópolis)

- Land parcel opportunities

- Payment plans up to 180 months (15 years)

Let me put this in perspective. A 10-year payment plan on an appreciating coastal asset, with no requirement for local credit history, is the kind of structure that simply does not exist in Miami or Lisbon at comparable price points.

How Payment Adjustments Work

Understanding how installments are corrected over time is essential for any serious investor.

During Construction — CUB: CUB (Custo Unitário Básico) reflects construction costs, including materials and labor. Installments adjust in line with those cost variations.

After Delivery — IPCA + Interest: IPCA is Brazil's official inflation index. Post-delivery, the remaining balance is adjusted by inflation plus a contractual interest rate. Given BRL volatility, I always recommend that USD-based buyers explore hedging strategies to manage currency exposure on these ongoing obligations. Never dismiss currency risk — it can erode returns just as quickly as appreciation can build them.

2. Traditional Bank Financing: Possible, but Complex

Bank financing in Brazil is available to foreign buyers, but it demands significantly more time and structure.

Typical requirements:

- CPF (Brazilian tax ID)

- Brazilian bank account

- Established financial relationship in Brazil

- Proof of income and/or assets

Long-Term (Relationship-Based): Building a financial profile over 12+ months through local investments, banking activity, and financial integration.

Short-Term (Asset-Based Lending): Using international assets as collateral — portfolio custody transferred to a Brazilian institution such as BTG Pactual, with loans issued at 30%–60% of asset value.

Key challenges:

- Higher bureaucracy and slower approval timelines

- Interest rates typically running 10%–15% per year

- Limited appetite from retail banks such as Itaú Unibanco, Bradesco, and Nubank

This route suits clients with strong financial profiles or long-term plans in Brazil. For these buyers, I strongly recommend structuring ownership through an LLC or trust for both liability protection and tax efficiency — it is one of the smartest moves you can make before capital ever crosses a border.

3. Consórcios: A Niche Alternative

A consórcio is a uniquely Brazilian model — essentially a savings pool rather than a traditional loan. A group of participants contributes monthly, and each month one or more members receive access to funds via draw or bid. There are no traditional interest charges, only administrative fees.

Pros: No interest rates (lower overall cost); flexible for long-term planning.

Cons: No guaranteed timeline to access funds; requires residency and financial integration; not suited for immediate acquisition; less accessible for non-residents.

For foreign buyers, consórcios are rarely the most practical option, though they can serve a role in specific long-term strategies.

The Bottom Line

Here's what the data actually shows: bank financing is possible but complex, consórcios are niche and slow, and developer financing remains the most efficient and accessible solution for international buyers entering the Santa Catarina market.

For absentee owners, I also want to be direct about the importance of professional property management — particularly if you plan to generate rental income while servicing a developer payment plan from abroad. The numbers only work if the asset is managed properly. I have seen too many investors optimize for acquisition and neglect operations.

If you are evaluating how Brazilian real estate fits into your broader portfolio allocation, I would encourage you to schedule a portfolio review with our team. We will walk you through specific opportunities in Florianópolis and across Santa Catarina that combine strong locations, flexible financing structures, and compelling investment potential. The arbitrage window won't stay open forever.